At Circle, we have long believed that the world’s economic infrastructure should have the speed and scale of the internet — a way for value to move as seamlessly as information. From our founding mission to raise global economic prosperity through the frictionless exchange of value, our work has focused on building a vertically integrated financial services technology solution: an open, programmable environment where trusted digital money and financial applications can operate natively on the internet.

In 2025, that vision came into sharper focus. The United States, Europe, Canada, Hong Kong, the UAE, and other jurisdictions enacted new, or began fully implementing existing, regulatory frameworks that recognize fully reserved digital currencies designed to maintain a stable value and onchain settlement as durable features of the global financial system.

Against this backdrop, Circle’s IPO was a defining step in our journey, reinforcing our long-standing commitment to transparency, strong governance, and rigorous risk management. Our recent conditional approval for a national trust charter further extends that commitment and signals our intention to operate at the core of regulated financial markets for digital money, strengthening institutions’, businesses’, and builders’ confidence in Circle’s technology.

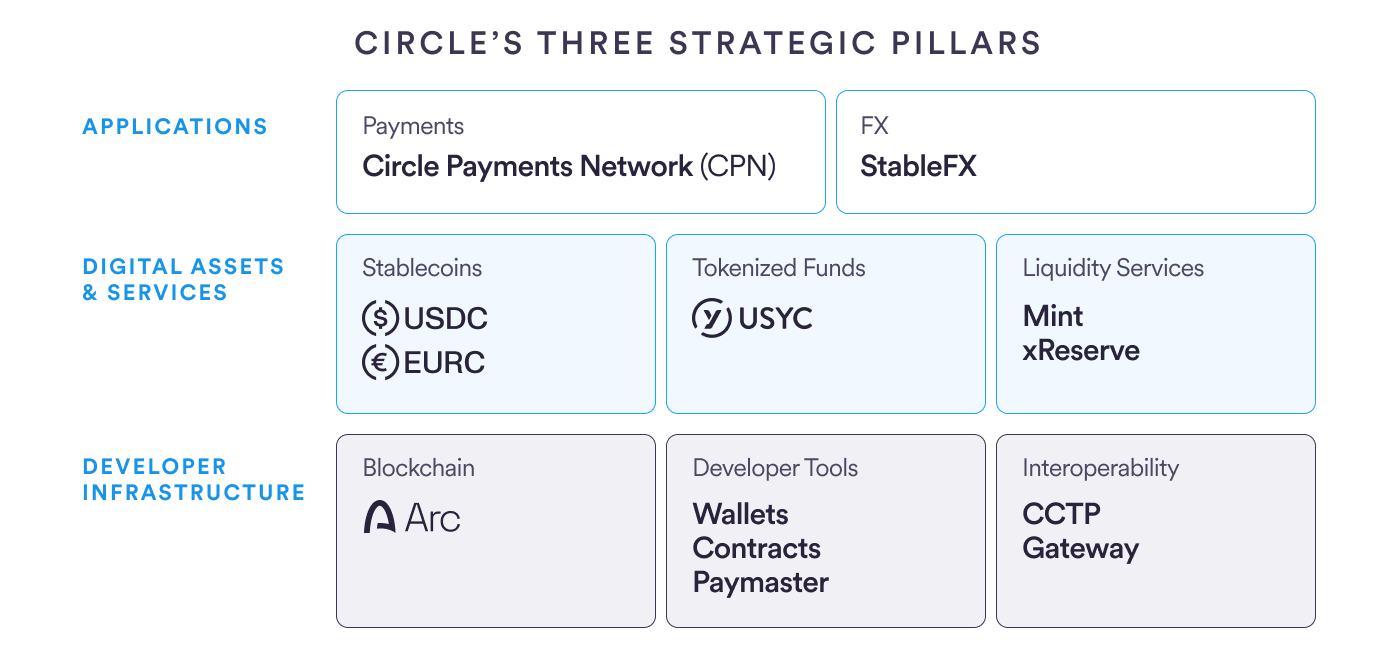

Our strategy rests on three mutually reinforcing building blocks that advanced sequentially throughout 2025. First, our fully reserved digital assets, USDC1 and EURC2, that function as programmable, internet-native forms of money, and USYC3, a tokenized money market fund (TMMF) providing institutional-grade, yield-bearing collateral. Second, a portfolio of applications and services, including Circle Payments Network4 (CPN) and Circle StableFX5, that make these digital assets accessible and usable to ecosystem participants around the world. And third, Arc6, the Economic OS for the internet — a purpose-built Layer-1 blockchain that unites programmable money and onchain innovation with real-world economic activity, designed to operate as neutral, institutional-grade infrastructure at internet scale. Together, these components — assets, apps, and infrastructure — represent Circle’s full-stack technology platform, which is moving programmable money and onchain commerce from the margins of experimentation to the mainstream of global finance.

Ultimately, what matters most is how our efforts can positively impact the world. Fast, low-cost remittances can help families keep more of what they earn. Improved cross-border payments can allow small businesses to pay suppliers in seconds instead of days. Programmable treasury and settlement tools can help financial institutions manage liquidity in real time and reach new markets more efficiently. We see these as signals of a broader shift toward an open, inclusive, and efficient internet-native financial system.

This Year in Review is organized around the key pillars of that shift in 2025. We begin with regulatory milestones and their role in unlocking significant commercial interest in onchain transactions with stablecoins. We then examine the growth and global reach of Circle digital assets as trusted, programmable dollars, euros, and tokenized cash instruments on the internet. Then, we highlight how applications and services are extending the real-world utility of our digital assets into payments, foreign exchange (FX), borrowing and lending, capital formation, asset tokenization, and more. And finally, we explore Arc as a new class of internet-native economic infrastructure — the Economic OS for the internet — designed to support the next generation of global financial activity.

Regulatory clarity unlocks adoption

A durable, full-stack platform for digital assets and infrastructure cannot thrive without clear, consistently applied rules and supervision. In 2025, the onchain regulatory landscape advanced substantially.

In July 2025 the GENIUS Act was signed into law in the US, providing the legal framework institutions, businesses, and builders needed to use fully reserved, transparent payment stablecoins as core components of modern financial infrastructure. The act aligned statutory requirements with Circle’s standards, including high-quality liquid reserves, predictable redemption, and rigorous compliance, and affirmed that regulated payment stablecoins will play a central role in the future of money and payments.

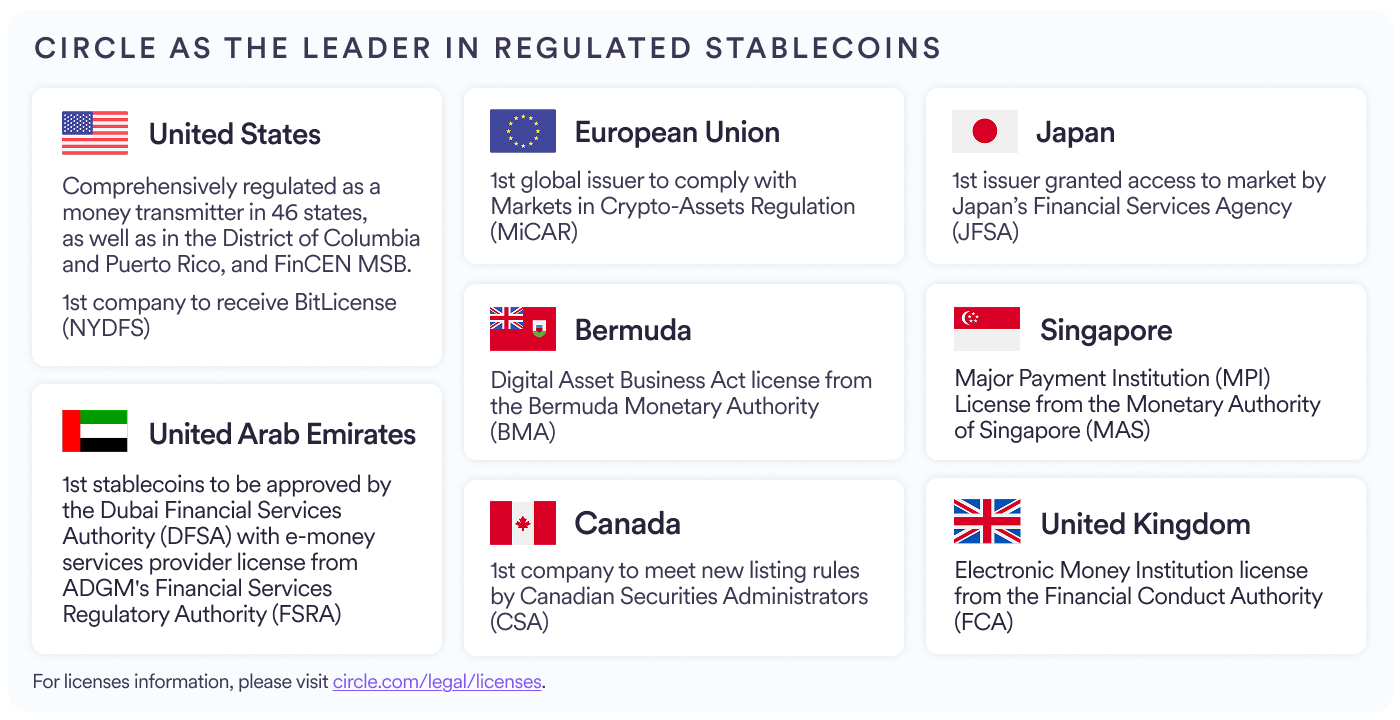

Subsequently, we also deepened our integration with the US banking system. Circle received conditional approval from the Office of the Comptroller of the Currency (OCC) to establish First National Digital Currency Bank, N.A., a proposed national trust bank that, once fully approved, would enhance the safety and regulatory oversight of the USDC Reserve, while enabling Circle to offer fiduciary digital asset custody and related services to institutional customers. This prospective trust bank is designed to provide institutions with an added layer of regulatory comfort and the knowledge that the reserves backing USDC are overseen by federal banking regulators.

Regulatory clarity has not stopped at US borders. In 2025, Circle remained the only major global issuer with both dollar- and euro-denominated stablecoins compliant with the European Union’s Markets in Crypto-Assets (MiCA) regime, positioning USDC and EURC as compliant digital assets across the 27-member bloc. In the Middle East, the Dubai Financial Services Authority (DFSA) recognized USDC and EURC as the first stablecoins approved under its crypto token regime, enabling thousands of firms in the Dubai International Financial Centre (DIFC) to integrate them into payments, treasury, and digital asset services. And, Circle secured a full Financial Services Permission (FSP) from Abu Dhabi Global Market’s Financial Services Regulatory Authority, allowing us to operate as a regulated money services provider and expand USDC-based payment and settlement tools across the UAE.

Circle also became a member of the Global Travel Rule (GTR) Network, expanding on its membership with the TRUST network, giving us the capabilities to support FATF Travel Rule-compliant transfers across a broader cohort of virtual asset service providers. These integrations are being woven into products such as CPN and Circle Gateway, so that banks, fintechs, and exchanges can inherit robust compliance coverage as part of their adoption of Circle’s platform. In effect, they make compliance an advantage for our customers, not just an internal obligation.

In parallel, industry participants have been assessing how to integrate USDC more deeply into their offerings, while the broader tailwind of digital asset regulation helped increase demand for EURC and USYC, Circle’s regulated TMMF. These developments reflected the beginning of a structural shift toward treating digital assets as scalable, mainstream, and resilient cash equivalents in the financial system.

A wave of commercial expansion

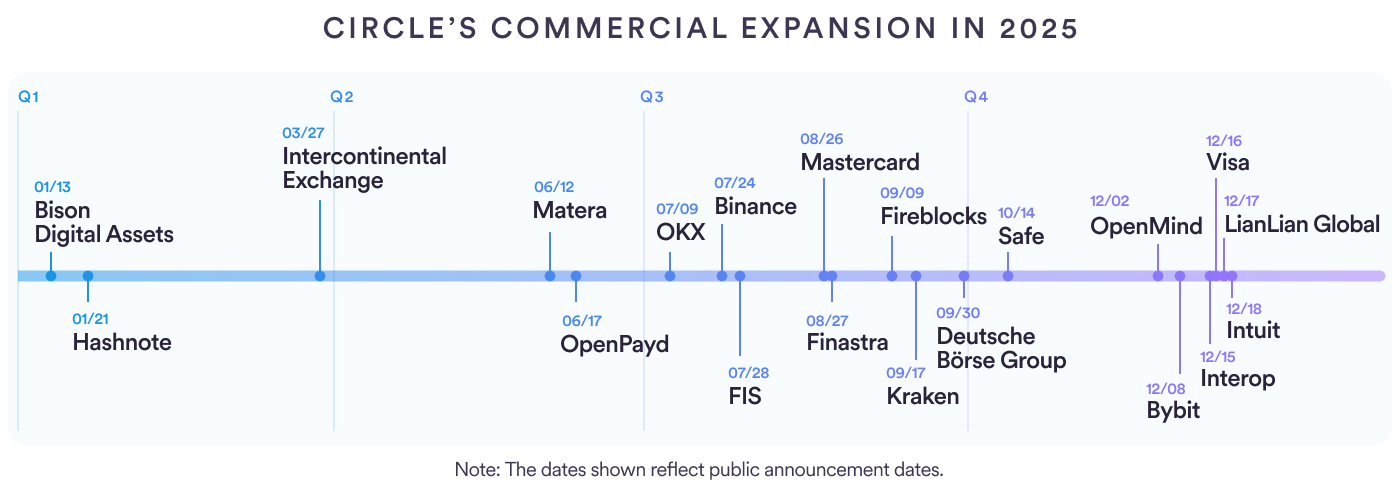

Regulatory clarity catalyzed a new phase of institutional engagement in 2025. Major market infrastructure providers continued to assess how USDC, EURC, and USYC could reduce settlement risk, compress operating windows, and unlock new products for clients.

In the US, Intercontinental Exchange (ICE), the operator of the New York Stock Exchange and one of the world’s leading exchange and clearing groups, committed to exploring the use of USDC and USYC in new products across its markets. This collaboration reflects a view shared by both firms: that regulated, fully reserved payment stablecoins and TMMFs can function as operational cash and collateral inside mainstream capital-markets workflows.

In the EU, Deutsche Börse Group, a leading European financial markets infrastructure provider, with Eurex, one of the world’s largest derivatives exchanges, committed to explore integrating USDC and EURC into trading, clearing, settlement, and custody flows to reduce settlement risk and increase operational resilience at the heart of European capital markets. This collaboration underscores that MiCA-compliant stablecoins are increasingly being treated as institutional-grade settlement instruments in European markets.

Financial services and fintech firms also seized the momentum created by clear rules and guidance from regulators. Finastra, whose software powers payments for many of the world’s largest banks, announced plans to integrate USDC settlement into its Global PAYplus platform, which handles trillions of dollars in daily cross-border flows. FIS, a financial technology company serving 95% of the world’s leading banks, plans to incorporate USDC into its Money Movement Hub. In doing so, it could open the door for more banks to offer stablecoin settlement through existing channels. And Intuit, the global fintech behind TurboTax, Credit Karma, QuickBooks, and Mailchimp, signed a multiyear partnership with Circle to leverage our stablecoin infrastructure across its entire platform.

We announced a commercial partnership with Matera, a Brazilian company which supports financial institutions’ integration of digital assets, to empower companies to more easily make cost-efficient and secure global payments. We also signed a memorandum of understanding with LianLian Global, a major fintech company specializing in cross-border payments, to explore opportunities in stablecoin-powered payment infrastructure for international markets. And Bison Digital Assets, the crypto asset subsidiary of Bison Bank, a private investment bank headquartered in Lisbon, worked with us to empower its customers to use USDC and EURC for deposits and withdrawals, conversions, and payments.

In addition, we teamed up with Visa to support the launch of USDC settlement in the US, allowing issuer and acquirer partners to settle with Visa in USDC. We expanded our existing partnership with Mastercard to enable both USDC and EURC settlement in the Eastern Europe, Middle East, and Africa region. And we partnered with OpenPayd, a financial infrastructure provider, to support its institutional clients’ access to seamless USDC and fiat conversions.

Cryptocurrency exchanges likewise moved to expand their engagement with Circle’s full-stack platform. Binance deepened its collaboration with Circle by supporting USYC as yield-bearing collateral for institutional clients, allowing them to use the TMMF as off-exchange collateral for derivatives trades. We solidified that relationship throughout the year, including with Binance holding its corporate treasury in USDC and expanding USDC access to reach more than 240 million Binance users around the world.

Bybit partnered with Circle to enhance USDC liquidity across spot and derivatives markets while further integrating USDC into its savings, cashback rewards, and everyday transactions products. Kraken accelerated the integration of USDC and EURC across its platform, giving customers increased liquidity, reduced conversion fees, and new opportunities to deploy USDC across its ecosystem. And, OKX introduced 1:1 USD/USDC and USDC/USD conversions for more than 60 million users, making it easier for its global user base to access the onchain economy.

The developer-facing Fireblocks meanwhile strengthened its custody and payments tooling by integrating Circle’s full-stack platform. Through the collaboration, Fireblocks customers gained access to Gateway and CPN, making it easier and safer for financial institutions to build digital asset offerings, execute cross-border treasury, and settle with stablecoins. Meanwhile, developers themselves — supported by Circle’s Developer Grants — are increasingly building onchain solutions geared toward solving legacy financial problems.

We also moved to strategically reinforce our infrastructure by entering into an agreement to acquire Interop. Expected to close in early 2026, the deal would bring Interop’s talent and technology directly into Circle, accelerating key initiatives across Arc and Cross-Chain Transfer Protocol (CCTP). This follows our early 2025 acquisition of Hashnote, which brought USYC into Circle’s full-stack platform, and our strategic partnership with Safe, which established our multisig-based smart account platform as a premier institutional storage solution for USDC in self custody and decentralized finance (DeFi).

At the frontier of innovation, we also began to see opportunities in new categories altogether. One such example is our collaboration with OpenMind to develop foundational standards for machine-to-machine payments. We believe that as AI agents begin to transact autonomously, demand for programmable, low-cost, high-throughput value exchange will grow. The speed at which stablecoins move make them an obvious match for high-throughput agentic commerce and could make machine-to-machine transactions viable at scale.

From cutting edge to foundational tool

The combined effect of these regulatory and commercial milestones is clear: regulated digital assets are moving from experimental tools at the edge of finance to foundational instruments integral to its core. GENIUS in the US, MiCA in Europe, DFSA recognition in Dubai, and new supervisory relationships with banking regulators are giving institutions the confidence to use Circle’s fully reserved stablecoins and tokenized funds as part of their core infrastructure, rather than as peripheral experiments.

The industry is now moving quickly to explore how Circle-issued digital assets can serve customers more effectively, modernize payment and settlement flows, and build new product lines for the onchain era.

Circle digital assets power global finance

The increased use of digital assets is seen clearly with USDC, EURC, and USYC. Over the course of 2025, USDC’s market capitalization expanded significantly, lifetime onchain transaction volume climbed higher into the tens of trillions of dollars, support broadened across dozens of blockchain networks, and our industry-leading liquidity continued to deepen. At the same time, EURC solidified its place as the largest euro-denominated stablecoin by market capitalization under Europe’s MiCA framework, while USYC has functioned as effective collateral management. Increasingly, these digital assets hold the potential to serve as foundational primitives for global finance — supporting payments and FX, streamlining treasury operations, serving as collateral, and more.

USDC sets the standard

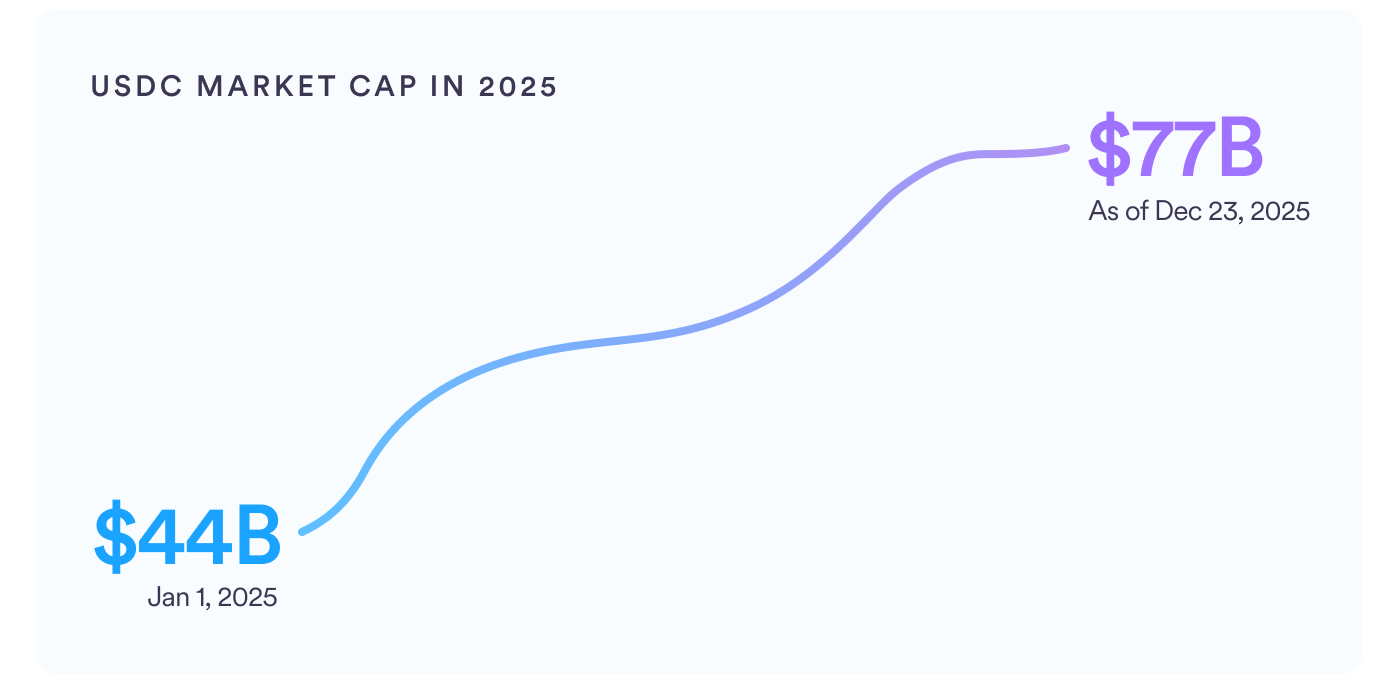

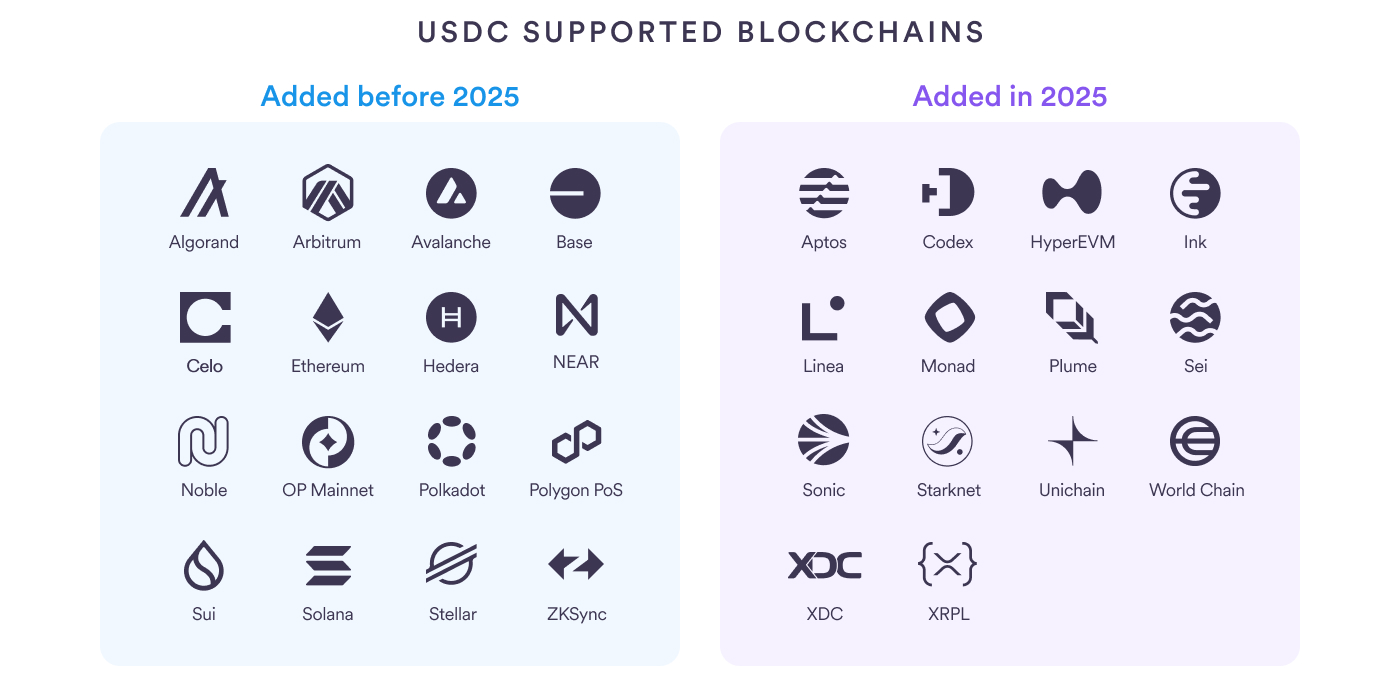

USDC had a standout 2025. Its market cap rose to $77 billion as of December 23, 2025, up from $44 billion on January 1, 2025, as adoption increased across crypto capital markets, institutional, enterprise, and consumer use cases. Native USDC was added to XRP Ledger, while native USDC and CCTP expanded to Aptos, Codex, Hyperliquid, Ink, Linea, Monad, Plume, Sei, Sonic, Starknet, Unichain, World Chain, and XDC Network, positioning USDC as canonical dollar liquidity on major Layer-1 (L1) and Layer-2 (L2) blockchains. Meanwhile, CCTP made USDC effectively “teleportable” across an increasing number of supported blockchains. That added crosschain functionality supported increased usage, which showed up in onchain data: as of December 23, 2025, USDC’s lifetime onchain transaction volume exceeded $50 trillion, with native support across 30 blockchains and CCTP enabling seamless crosschain flows of USDC.

Liquidity also meaningfully deepened over the year, reflecting a material strengthening of USDC’s role in market infrastructure. Across leading exchanges, USDC liquidity has improved dramatically. On Binance, for example, USDC spot liquidity in the BTC/USDC pair increased by 227%, with comparable trends across ETH/USDC and SOL/USDC. Perpetual markets demonstrated even more pronounced expansion, with BTC/USDC depth increasing by more than 200% within the same pricing band. This progress coincided with a marked rise in open interest and sustained growth in daily trading volumes, during which USDC’s open interest on Binance increased three times relative to USDT year to date. The scale and persistence of these changes highlight that USDC is closing the gap relative to USDT in terms of market depth, turnover, and trader engagement.

Spreads tightened accordingly. In both January and November (the most recent month as of writing), USDC traded on major exchanges with spreads under 1 basis point 99% of the time, including during periods of heightened market volatility. This performance indicates a measurable strengthening of market resilience and execution quality. Slippage on a $100,000 BTC/USDC trade declined from 42 basis points in January to less than 5 basis points by November, demonstrating that traders could reliably execute larger transactions with limited market impact.

These developments reinforced USDC’s existing structural advantage — gained from Circle’s USDC reserve transparency and regulatory alignment — and helped to position USDC as the asset underpinning high-integrity liquidity across the emerging internet-native financial system.

EURC meets growing demand

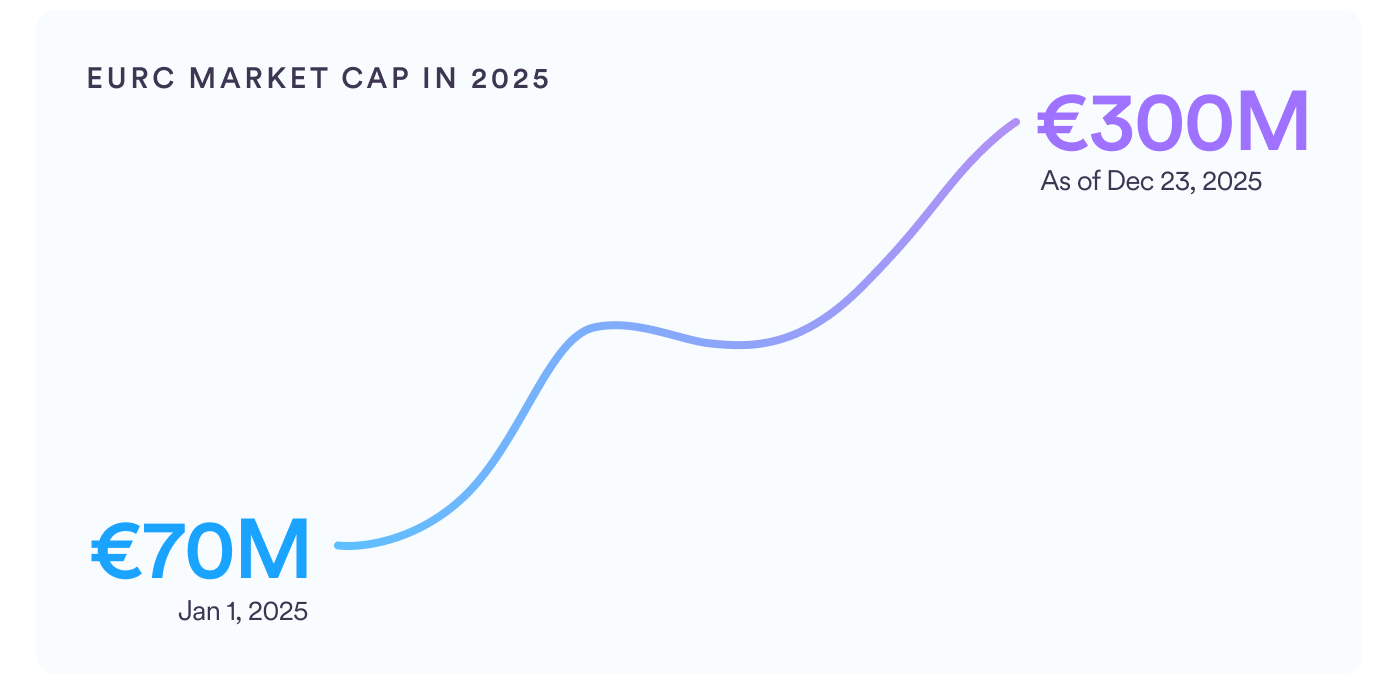

2025 was also a pivotal year for EURC. As European institutions came under the clarity of MiCA, demand grew for a fully reserved, transparent, euro-denominated stablecoin. EURC’s market cap rose to more than €300 million as of December 23, 2025 up from approximately €70 million on January 1, 2025, making EURC the largest euro-denominated stablecoin by market cap as of this writing.

Contributing to that growth is EURC’s expansion to World Chain, an L2 blockchain built on the OP Stack. The addition unlocked deepened EURC liquidity across World Chain and brought EURC to the more than 37 million World App users, enabling buy, sell, and send flows for everyday euro transactions. This combination of regulatory compliance, institutional on/offramps, and consumer-facing distribution reinforced EURC as a credible euro-denominated counterpart to USDC in both payments and DeFi.

EURC’s trajectory points toward a future in which trusted digital assets denominated in local currencies serve regional needs, such as eurozone commerce, while still participating in global financial flows including FX. It is a concrete example of how internet-native money can align with local regulatory regimes and currency preferences, without sacrificing global interoperability.

USYC accelerates tokenized money market fund adoption

Alongside USDC and EURC, USYC, Circle’s TMMF, continued to gain traction. USYC’s assets under management increased by approximately $592 million between November 1 and December 23, 2025, increasing from $948M to $1.54B — making USYC the second-largest TMMF globally.

The movement was driven in part by USYC’s expansion to BNB Chain, a high-performance blockchain with an active builder community and deep liquidity. This addition meant developers could use USYC as programmable, yield-bearing collateral in the DeFi venues they already relied on, with near-instant settlement in USDC. In addition, USYC’s addition to Solana upped the number of blockchains supporting the TMMF and brought the digital asset to a blockchain engineered for low-latency transaction confirmations and high throughput.

Institutions use USYC as a way to hold exposure to short-duration US Treasuries while retaining the 24/7 flexibility of onchain settlement. Near-instant redemptions into USDC allow treasury teams and traders to move between yield-bearing assets and stablecoin liquidity in real time. That capability is highly valued and difficult to replicate in traditional markets. In effect, USYC helps to bridge conventional fixed-income strategies and programmable, internet-native liquidity.

Transparency, trust, and clarity

Transparency and strong regulatory alignment became powerful drivers of adoption in 2025. Circle’s regulatory-first approach provided institutions, businesses, and builders the confidence to adopt USDC, EURC, and USYC. As the onchain economy matures, the divide between digital assets designed as secure stores of value and those that fall short is becoming increasingly pronounced. We are seeing digital assets that are designed to maintain a stable value become primitives for innovation, forming the monetary and collateral layer of an emerging internet-native economic system.

Applications and services turning digital assets into real-world solutions

With a growing family of regulated digital assets in place, 2025 was about making those assets more usable for real-world financial workflows. That meant building applications and services that let institutions use USDC, EURC, and USYC as operational tools for payments, FX, treasury, settlement, and more. CPN, CCTP, Gateway, Circle xReserve, Mint, StableFX, Circle Wallets, and other supporting applications and services are now the connective tissue that turns digital assets into everyday financial infrastructure.

Accelerating global money movement with Circle Payments Network

The existing cross-border payments system, built on a decades-old correspondent banking model, has struggled to keep pace with the expectations of an internet-native economy. Settlement delays, high fees, inconsistent reach, and operational fragmentation characterize the reality of many cross-border payments flows for financial institutions and their customers.

In response, we introduced CPN, a global, stablecoin-powered payments network that serves as an orchestration layer for duly licensed financial institutions to make real-time payments. Launched in early 2025 with more than 25 design partners, CPN uses stablecoins like USDC and EURC to facilitate predictable, internet-native settlement without traditional intermediaries. CPN offers a one-to-many integration, enabling participants to expand their global reach by connecting to just a single API. We also focused on the institutional onboarding experience by adding CPN Console, a self-service interface designed to streamline onboarding and technical integration into a single, unified experience.

CPN enables financial institutions to deploy cross-border payments using familiar processes (like a Request for Quote, or RFQ, system), but with an added onchain component that unlocks a new level of flexibility, control, and performance. CPN’s operational rules framework lets participating institutions define custom risk controls (e.g., transaction limits, country and corridor policies, and counterparty rules) and have those enforced programmatically across the network. Instead of renegotiating bilateral terms or rebuilding integrations every time policies change, participants can update their internal rules within CPN and immediately reflect them in onchain payment behavior. CPN’s design also anticipates the realities of modern compliance. Integrations with Travel Rule networks and Circle’s broader compliance stack allow participants to inherit robust sanctions and Travel Rule coverage as part of their CPN connectivity, rather than stitching these capabilities together themselves.

Early CPN use cases highlight the breadth of demand for faster, more reliable global financial flows. Partners are using CPN to gain advantages like B2B trade payments that can settle in seconds rather than days, remittances delivered nearly instantly to families worldwide, always-on treasury and liquidity flows for global enterprises, and humanitarian disbursements that reach communities more quickly during critical moments.

CPN partners like Alfred and Tazapay are already processing real cross-border flows on the network. For Brazilian markets, Alfred enables USDC to be converted to BRL and paid out via Pix almost instantly, reducing traditional FX friction and delays. In Asia-Pacific, Tazapay demonstrates how USDC, via CPN, can be converted to local currency and deposited directly into bank accounts, transforming cumbersome correspondent bank payouts into near-instant disbursements.

With institutions already live on the network and more in the pipeline, CPN is advancing critical payments infrastructure and breaking down technical and operational barriers for businesses seeking the benefits of onchain settlement. What began the year as a new product launch is ending it as an active, multi-participant network — one that functions like a modern counterpart to card and correspondent systems, but with programmable guardrails and real-time settlement built in.

Expanding liquidity and interoperability with Mint, CCTP, Gateway, and xReserve

As real-world digital asset use grew in 2025, Circle continued to expand the liquidity and interoperability foundation required to support that growth.

Circle Mint7 provides institutions with direct access to USDC and EURC issuance and redemption, enabling a consistent, multichain liquidity experience backed by a single global issuer. This year we made improvements to Mint’s fee structure UX, made it possible for Mint users to manage multiple accounts with unified login credentials, and established self-serve access to Mint’s core APIs, helping to streamline and expedite the onboarding process for new customers. We also enabled USDC/EURC conversions (and vice versa) directly within Mint, enabling users to convert between these assets 24/7 at competitive FX rates.

USDC, natively available on 30 blockchains as of December 23, 2025, sets a high standard for the type of crosschain liquidity a stablecoin needs to be widely adopted across the industry. Notably, 14 of those networks were added in 2025 alone, underscoring the rapid expansion of the multichain foundation that institutions, businesses, and builders seek. As Circle’s digital assets like USDC expanded across more chains in 2025, we invested heavily in making that multichain footprint an operational advantage rather than a source of fragmentation. CCTP, Gateway, and xReserve together form the backbone of this effort.

CCTP, originally launched in 2023 and upgraded in March 2025, is our burn-and-mint protocol that enables end users to transfer native USDC across 17 supported blockchains as of December 23, 2025. CCTP has processed more than $126 billion in cumulative volume, and more than 6 million total crosschain transfers.8 This means USDC can move seamlessly through the onchain ecosystem while taking advantage of different chains’ performance, cost, and distribution strengths. This functionality has made CCTP one of the most widely integrated interoperability protocols in the industry, underpinning crosschain bridging infrastructure like Interport, LI.FI, SOCKET, Stargate, Wormhole, and others. And we’ve made it easier than ever to integrate CCTP into applications with Bridge Kit, a developer toolkit that makes key CCTP operations available as high-level software development kit (SDK) methods so builders can integrate crosschain USDC transfers in under 10 lines of code. (Builders can find Bridge Kit and other Circle SDKs in a single resource using our newly launched SDK Explorer.)

Gateway complements CCTP by abstracting crosschain complexity. Gateway provides a unified USDC balance that, as of December 23, 2025, is easily accessible across 11 supported blockchains — Arbitrum, Avalanche, Base, Ethereum, HyperEVM, OP Mainnet, Polygon PoS, Sei, Sonic, Unichain, and World Chain — without manual bridging and in less than a second. For exchanges, custodians, PSPs, and wallets, this transforms multichain USDC from a series of siloed pools into a single, fluid liquidity resource that can be deployed wherever customer demand arises, without manual rebalancing. Providers such as Blockradar, Daimo Pay, Eco, Enclave Money, and RockawayX are already using Gateway to simplify multichain experiences for their customers.

xReserve enables blockchain teams to deploy USDC-backed stablecoins on supported chains that don’t offer native USDC. These USDC-backed assets remain fully interoperable with USDC across supported chains via CCTP and Gateway. Depositing funds in Circle xReserve, rather than a third-party bridge smart contract, reduces the additional trust assumptions typically introduced by external bridging layers. USDCx on Canton became the first production example of this model, allowing the blockchain to support a USDC-backed stablecoin tightly integrated with existing institutional workflows. Aleo, an L1 blockchain built for privacy-focused applications using zero-knowledge proofs, then launched a USDC-backed stablecoin on Aleo Testnet to enable confidential transactions with built-in compliance hooks. Stacks, an L2 that brings smart contracts and decentralized apps to the Bitcoin network, also launched a USDC-backed stablecoin in late 2025 to enable developers to build Bitcoin-secured apps using an interoperable stablecoin. These deployments demonstrate how USDC-backed stablecoins can tailor privacy, performance, and regulatory posture to the needs of specific ecosystems while maintaining a unified liquidity backbone.

Taken together, Mint, CCTP, Gateway, and xReserve help establish an entirely new UX for digital dollars. From a balance sheet perspective USDC is one asset (even as distinct versions of USDC exist across a growing ecosystem of chains and settlement environments), helping more market participants operate onchain with flexibility and confidence.

Reimagining global currency conversion with Circle StableFX

While Mint, CPN, CCTP, Gateway, and xReserve in concert focus on payments, liquidity, and interoperability, StableFX and Circle Partner Stablecoins address another important aspect of cross-border finance: foreign exchange. Global businesses need fast, transparent, and cost-efficient ways to convert between currencies. In November 2025, Circle announced StableFX, an institutional-grade FX engine that combines familiar RFQ-style execution with onchain settlement in a market that sees more than $10 trillion in daily volume.

StableFX, now live on Arc Public Testnet, is designed to give institutions access to stablecoin-based currency pairs with 24/7, capital-efficient settlement — compressing what has traditionally been a T+1, prefunded, and venue-fragmented process into near-real-time onchain flows. StableFX is purpose-built to work alongside Circle Partner Stablecoins, a program that supports regional issuers in bringing new fiat-linked stablecoins onto shared infrastructure.

In this model, USDC and USDC-backed assets provide the reserve layer, regional stablecoins represent local currency access, and StableFX acts as the programmable FX fabric connecting them. Global stablecoin issuers supporting StableFX include Avenia (BRLA), BDACS (KRW1), Coins.ph (PHPC), Forte (AUDF), Juno (MXNB), JPYC (JPYC), Stablecorp (QCAD), and the ZAR Universal Network (ZARU), with initial collaborations underway. Early participants illustrate how local issuers can plug into this framework and tap into a global, stablecoin-native FX infrastructure rather than building one from scratch.

The long-term vision is clear: a multi-currency network where eligible dollar- and euro-denominated, and local stablecoins can be exchanged and settled programmatically, around the clock, on a platform designed for institutional risk and performance requirements.

Wallets and autonomous payments: from user flows to AI agents

Wallets are how users interact with the onchain world; this crucial infrastructure is where end-user experiences, developer workflows, and emerging agentic use cases converge. Circle Wallets — our wallet-as-a-service platform — gives developers secure, flexible infrastructure to embed USDC wallets directly into applications, supporting both developer-controlled and user-controlled models. And, new in 2025, we launched Modular Wallets, a new deployment option that gives developers even greater control over designing app experiences.

With Wallets, developers can embed financial flows directly into their applications and unlock the benefits of onchain programmability, reach, and efficiency without complicating the end user experience. Gas Station, for example, enables developers to pay network fees on behalf of users, making stablecoin transactions feel as seamless as the experience in traditional apps. Also new in 2025 is Circle Paymaster, which allows users to pay gas fees in USDC instead of a network’s potentially volatile native gas token for a more predictable experience.

This year we also extended our wallet infrastructure into a new domain: autonomous, machine-to-machine payments. Through our work with Coinbase’s x402 protocol and collaborators such as OpenMind, Circle integrated developer-controlled wallets with x402 to enable AI agents to pay for API access, data, compute, and content autonomously using USDC. This effectively brings the long-dormant HTTP 402 “Payment Required” status code to life, allowing onchain payments to be embedded directly into standard web requests.

For businesses, this opens up new possibilities: pay-per-use access to services without prefunded accounts, dynamic pricing for AI workloads, and programmable spending policies for autonomous agents — all supported by the same stablecoin infrastructure that underpins human-driven payments. Wallets, x402, and Arc together form a blueprint for how stablecoins can power both today’s user experiences and tomorrow’s AI-native commerce.

Across CPN, Mint, CCTP, Gateway, StableFX, Wallets, and related tooling, 2025 marked the transition from standalone products to an integrated services layer. This layer is what makes Circle’s digital assets function as software primitives that institutions can compose: a payments network with programmable rules, crosschain liquidity as a service, FX as an onchain engine, and wallets that can serve both people and agents.

Real-world adoption and impact

The true measure of progress in 2025 wasn’t the breadth of our product stack or the global rollout of clearer regulatory frameworks, but what builders and customers were able to accomplish because of them. Across consumer banking, cross-border payouts, payroll, small-business finance, and remittances, we saw Circle’s assets and apps move from pilots and proofs of concept into services that increasingly shape people’s financial lives.

Extending the utility of Circle digital assets with a community of builders

Institutions, businesses, and builders are actively extending Circle’s tools and capabilities into new use cases. This proliferation is in part driven by the Circle Alliance Program (CAP), a global network of businesses and builders using USDC and other Circle tools to create real-world financial applications. Launched in 2024, CAP now has 1,065 members as of December 2025.

CAP members are expanding remittance corridors, embedding stablecoin settlement into commerce and payroll platforms, enabling new forms of cross-border credit, exploring machine-to-machine payment models, and more. Their work is driving momentum for the broader internet economy and demonstrating how an ecosystem of innovators can multiply the impact of core infrastructure and assets.

Mainstream distribution: digital dollars for everyday savers

In Latin America and outside of CAP, this shift was highlighted in our work with Nubank, one of the largest digital banks in the world, serving 127 million customers across Brazil, Mexico, and Colombia. By integrating USDC into its platform, Nubank began giving tens of millions of Brazilians a simple way to access and hold digital dollars inside Nubank’s app. For everyday users, the benefit is straightforward: the ability to protect a portion of their savings in a dollar-denominated instrument without opening a foreign bank account, wiring funds offshore, or navigating crypto-native interfaces.

This partnership encapsulates the role we aspire to play in emerging markets: Circle provides the fully reserved, regulated1 digital dollar and serves as a technology partner; Nubank provides the distribution, user experience, and local regulatory compliance; and together we deliver a product that feels as intuitive as any traditional savings feature. For Circle, it is a flagship example of how a single, interoperable asset, USDC, can underpin mass-market access to digital dollars through trusted local institutions.

Cross-border payouts and remittances: from T+2 to always-on

Cross-border payments remain one of the most painful parts of the existing financial system. In 2025, several partners began to show what it looks like to replace multi-day correspondent flows with always-on, stablecoin-based settlement.

Thunes, a global payments network connecting hundreds of financial institutions, wallets, and alternative payment methods, worked with Circle to use USDC as an always-on settlement asset. Instead of prefunding accounts across multiple currencies and time zones, Thunes can increasingly use USDC as a neutral, programmable tool for moving value between institutions in near-real time. For their customers, this translates into faster settlement, lower working-capital drag, and fewer reconciliation headaches.

At the other end of the spectrum, Lipaworld, a stablecoin-powered neobank, demonstrated how the same infrastructure can power deeply human use cases. By combining USDC with a digital voucher marketplace, Lipaworld enables migrant workers and freelancers to send value home and pay small businesses in a way that is faster, more transparent, and more empowering than traditional remittance channels. Here, the “infrastructure story” shows up as something quite tangible: a higher share of each paycheck reaching the people and businesses it was intended to support.

Together, these examples illustrate why we believe always-on, stablecoin-based settlement is not a niche alternative, but a superior model for cross-border value transfer, whether the counterparty is a global payouts network or a neighborhood merchant.

Global payroll and workforce finance

The nature of work is increasingly global, remote, and flexible. Payroll infrastructure has been slower to change. In 2025, partners such as Rise used USDC to close that gap, enabling companies to pay distributed teams more quickly and reliably than is possible with traditional rails.

By settling in USDC, employers can reduce reliance on complex, multi-currency bank corridors and intermediaries, while workers can receive value in a digital dollar that is easily convertible into local currency or spendable directly where supported. For contractors and freelancers, this can mean saving days in payment time and more predictable access to earnings; for employers, it can mean simplified treasury flows and fewer operational bottlenecks in scaling globally.

We see this as a template for a new category of “internet-native payroll", where high-integrity stablecoins and programmable payouts infrastructure replace the patchwork of bank transfers and manual processes that characterize global workforce payments today.

Mission and inclusion: Circle Foundation and impact initiatives

As our commercial and institutional footprint expanded in 2025, we also took steps to formalize our long-standing commitment to financial inclusion and resilience. Through Pledge 1%, Circle seeded the newly formed Circle Foundation, a donor-advised fund, with Circle equity, establishing a dedicated philanthropic vehicle to support initiatives aligned with our mission to raise global economic prosperity.

The Foundation’s mandate is to fund and support efforts that make financial systems and tools more accessible, especially for communities that are underserved by traditional systems. Onchain products and services are becoming the tools that families use to save, workers rely on to get paid, small businesses use to manage cash flow, and institutions use to move capital more efficiently across borders. Through the Foundation, our ongoing policy work, and ecosystem-building efforts, inclusion is a core design principle of the infrastructure we are building, not just a by-product of growth.

Arc: The Economic OS for the internet

With trusted digital assets and an applications layer in place, 2025 was the year we introduced Arc, an open, EVM-compatible, L1 blockchain purpose-built to support real-world economic activity. Most existing blockchain networks were not designed for the performance, predictability, and compliance requirements global businesses demand. To support the kind of high-volume, always-on, real-time financial activity envisioned in our long-term strategy, the world needs internet-native infrastructure that is both open and institutional-grade — effectively, an economic operating system tailored for lending, capital markets, FX, and payments. Arc is designed to play that role as the Economic OS for the internet.

Circle acquired the Malachite team from Informal Systems (creators of the Malachite consensus engine, a key part of Arc’s ultimate design) earlier in the year and launched the Arc Public Testnet in October. The launch brought more than 100 launch and design participants into a shared effort to build the next generation of onchain economic infrastructure. Organizations committed to building and testing on Arc span the full spectrum of global finance. They include major asset managers (such as BlackRock, Deutsche Bank, Goldman Sachs, HSBC, and Standard Chartered); capital markets firms (including Apollo, BNY, NYSE / ICE, and State Street); technology and payments companies (such as AWS, Mastercard, Nuvei, Visa, and WorldPay); leading crypto exchanges and service providers (including Coinbase, Fireblocks, Kraken, Ledger, MetaMask, and Robinhood); and stablecoin issuers across Asia, Latin America, and beyond. These participants are exploring use cases spanning credit markets, capital markets, FX, treasury flows, programmable commerce, and payments.

Engineered for economic activity, natively connected to Circle liquidity and services

Arc is designed around the needs of real-world economic activity. It’s built from the ground up to support a broad spectrum of financial workflows with core features like deterministic sub-second finality, fiat-denominated and predictable fees, and configurable privacy tooling. These design choices position Arc as enterprise-grade network infrastructure that supports settlement, liquidity movement, and programmable financial workflows with the predictability treasury and operations teams expect.

Arc’s role in the broader platform is to sit downstream of Circle’s digital assets and applications, providing the economic foundation on which trusted digital assets and real-world financial applications operate. Arc uses stablecoins like USDC as native gas to enable predictable dollar-based fees, and it is designed to integrate directly with Circle applications such as StableFX, CPN, and other services.

Supporting AI agents and autonomous commerce

In 2025, we worked with participants across the ecosystem to demonstrate how AI agents, USDC, and zero-knowledge proofs can combine on Arc to power new forms of autonomous, trust-minimized finance.

Through the AI Agents on Arc with USDC hackathon and workshop series, for example, developers around the world explored how to use USDC, Wallets, and Arc to build agents that can understand natural-language instructions, execute financial actions, and pay for APIs, data, and compute autonomously. Community projects extended these ideas into concrete applications, such as an AI-powered disaster-relief portal that uses Arc and USDC to distribute aid via autonomous agents, with zero-knowledge verification enabling funds to reach eligible recipients transparently and with reduced fraud risk. The Arc Community Hub’s Next Internet Economy series distilled these efforts into a broader thesis: that a new internet economy is emerging where AI agents, stablecoins, and onchain infrastructure form a continuous loop of earning, spending, and settling value.

Other community events for Arc this year included a DeFi hackathon in London and Arc Studio, a developer meetup that took place at Devconnect Argentina. For Circle, these early community events (and resulting onchain experiments) are proof points that Arc can support entirely new categories of financial activity alongside traditional financial flows.

Spurring growth in the Arc ecosystem

Developer momentum around Arc accelerated throughout 2025. As of December 2025, Arc’s Discord community grew to more than 20,000 “Architects", and we hosted more than 20 Arc-focused online workshops and technical discussions to support builders. Early signals of adoption are already visible, with the community surfacing a meaningful pipeline of projects built or underway across a range of onchain financial use cases.

Arc’s momentum is further reinforced by Circle’s community and grants initiatives, like the recently announced Arc Builders Fund, which is designed to support developers building foundational tools and applications. Early grantees are working on compliance primitives, institutional liquidity tools, and enterprise-grade financial applications, helping to strengthen the broader ecosystem and demonstrating Arc’s versatility as infrastructure for both established institutions and emerging builders. These contributions are accelerating adoption, expanding real-world utility, and supporting Arc’s evolution as a robust, globally relevant Economic OS for the internet.

An emerging platform for an inclusive global economy

Arc is still early; 2025 was the year of public testnet, core protocol hardening, and onboarding the first wave of builders and institutional design partners. But the contours of its role are already visible: it is the economic environment where trusted digital assets and the next generation of financial applications can converge. For Circle’s applications like CPN and StableFX, Arc provides a purpose-built environment optimized for high-speed settlement with configurable privacy tooling. For those building on Arc, it offers a foundation on which to design new financial services that expand what is possible onchain across lending, capital markets, FX, and payments.

Taken together with the regulatory progress, asset expansion, application layer, and real-world adoption outlined earlier in this Year in Review, Arc represents the next logical step in our mission: delivering an enterprise-grade Economic OS for the internet — a neutral foundation where trusted digital assets, real-world financial applications, and intelligent agents can operate and coordinate at global scale. As we look beyond 2025, we plan for Arc to bring us closer to a world where users worldwide can participate more fully in the global economy through fast, affordable, and open access to financial services.

Looking ahead: The internet financial system

The progress we made in 2025 is just the beginning. The world is still early in the transition from decades-old financial infrastructure to an internet financial system — one where value exists online natively and can move faster than ever before. The regulatory clarity achieved in key markets, the growth and diversification of trusted digital assets, the expansion of applications with real-world utility, and the early momentum of blockchain infrastructure purpose-built for real world economic activity all point to a future in which programmable, onchain finance plays a foundational role in the global economy.

For years, we have invested in our mission to raise global economic prosperity through the frictionless exchange of value by building trusted digital assets, resilient infrastructure, and an ecosystem of partners around them. We are committed to continue playing a constructive role as a neutral issuer of trusted digital money, a builder of institutional-grade infrastructure, and a partner to those creating the next generation of financial applications. The work we undertook in 2025 — from advancing regulatory milestones and launching new products to driving ecosystem growth and infrastructure innovation — marked a pivotal validation of that hard-fought approach. As we look ahead, we are focused on scaling this impact, ensuring that the benefits of an open, inclusive, and efficient internet financial system reach ever more people around the world.

Disclosures:

Reference to any specific company, product, service, or website of any third party does not constitute an implied or express endorsement, recommendation, favoring or validation by Circle. The content presented is intended for informational purposes only. Reliance upon any content or information presented is at the sole discretion of the audience; Circle shall not be liable for any damage or loss relating to the use of or reliance upon any such content or information presented. The views and opinions of others expressed herein do not necessarily state or reflect those of Circle.

Forward-Looking Statements

This document contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact are forward-looking statements. The words “believe,” “may,” “will,” “estimate,” “potential,” “continue,” “anticipate,” “intend,” “expect,” “could,” “would,” “project,” “plan,” “target,” and similar expressions are intended to identify forward-looking statements. Forward-looking statements are based on management’s expectations, assumptions, and projections based on information available at the time the statements were made.

These forward-looking statements are subject to a number of risks, uncertainties, and assumptions. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties, and assumptions, our actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements. Further information on risks that could cause actual results to differ materially from forecasted results are, or will be included, in our filings we make with the SEC from time to time, including our Quarterly Report on Form 10-Q for the quarter ended September 30, 2025 filed with the SEC on November 12, 2025. Except as required by law, Circle assumes no obligation to update these forward-looking statements, or to update the reasons if actual results differ materially from those anticipated in the forward-looking statements.