01

|

USDC e os ativos digitais da Circle

Stablecoins regulamentadas como o USDC estão ajudando a impulsionar a criação de um novo sistema financeiro da internet, que está fazendo pelo dinheiro o que as gerações anteriores de inovação na internet fizeram pelos dados, pelas comunicações e por outros setores. Com o tempo, esperamos que esse novo sistema reformule a maneira como empresas, instituições e bilhões de pessoas interagem com recursos financeiros no dia a dia.

As stablecoins formam uma camada híbrida entre as finanças tradicionais e a infraestrutura on-chain. Integram redes isoladas, eliminam atritos estruturais, aumentam a eficiência do capital, ampliam o acesso e apoiam a inovação financeira responsável. As stablecoins oferecem aos bancos, empresas de pagamento, corporações e instituições uma oportunidade significativa de aprimorar sua maneira de operar e agregar valor para seus clientes e partes interessadas.

O resultado dessa modernização das finanças será muito mais do que apenas uma melhor infraestrutura financeira subjacente: servirá de base para serviços financeiros mais dinâmicos, adaptáveis e inclusivos no mundo inteiro. Ao aumentar radicalmente a velocidade e a escala das formas tradicionais de dinheiro e introduzir novas propriedades como a programabilidade, as stablecoins regulamentadas podem aprimorar as finanças globais de forma significativa. Essa transformação tem o potencial de desbloquear níveis inéditos de prosperidade, participação e coordenação econômica global.

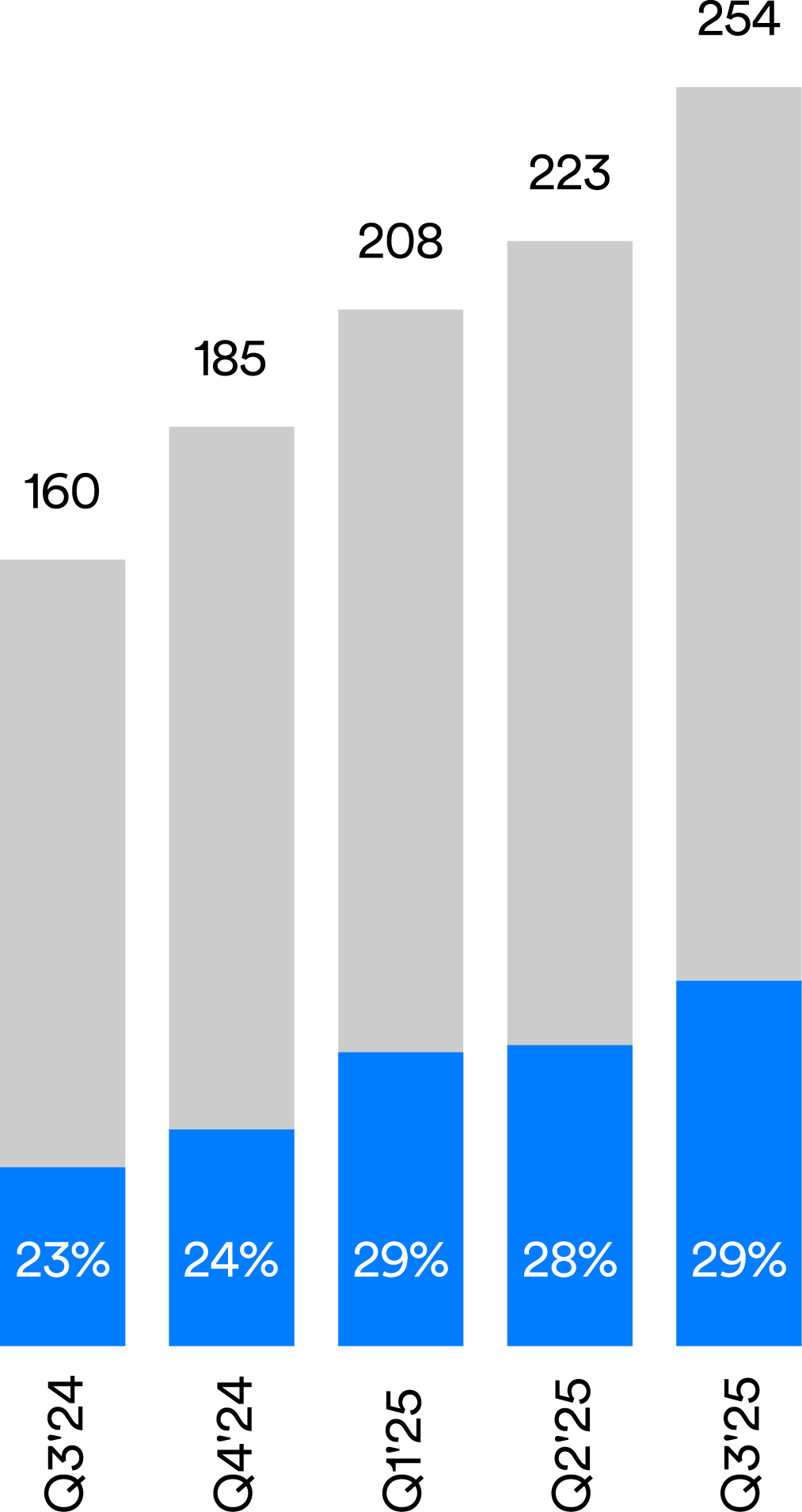

Participação do USDC no volume de stablecoins em circulação⁴

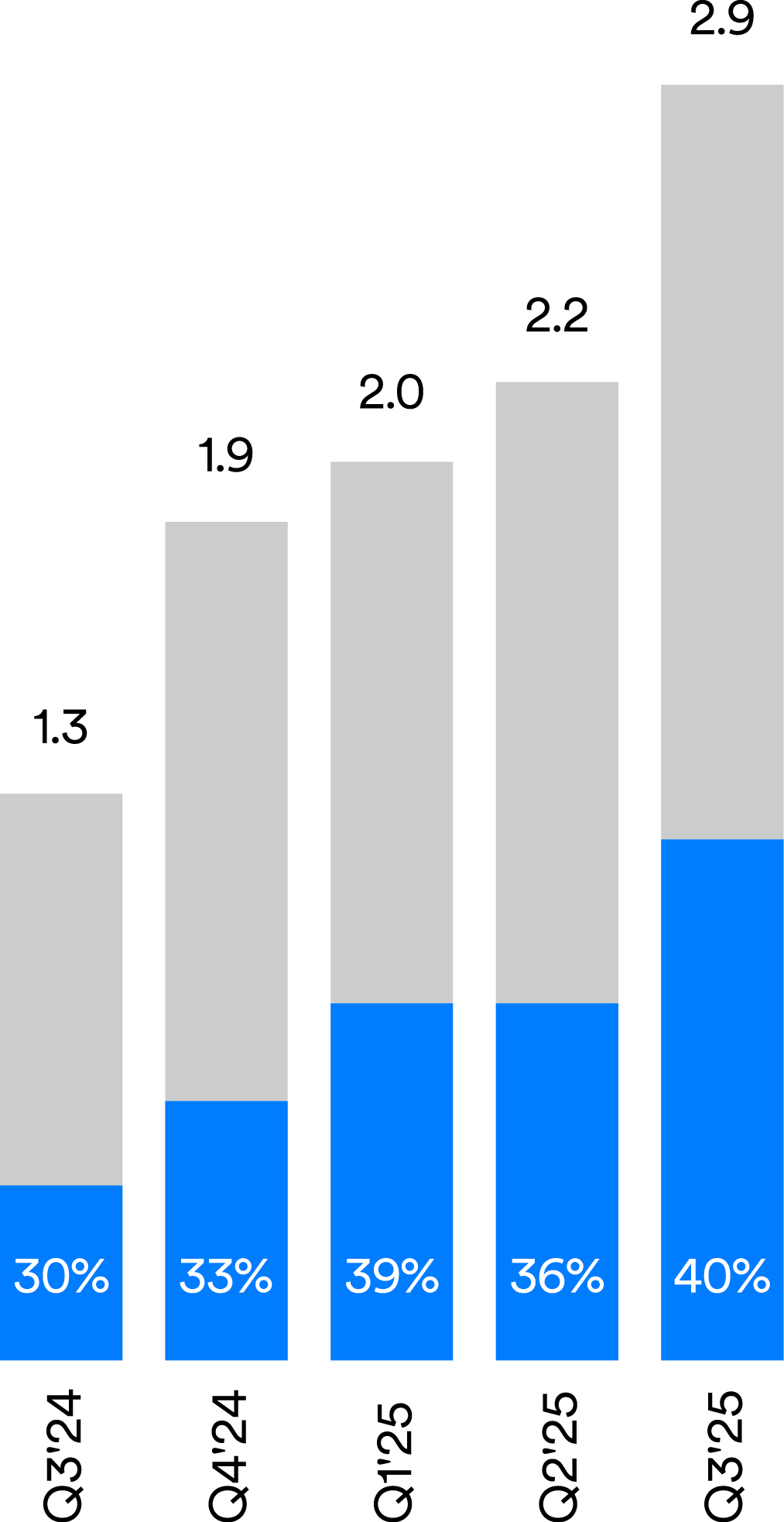

Participação do USDC no volume de transações de stablecoins⁵

Liquidações on-chain que o USDC possibilitou⁶

Hoje, o USDC atua como uma sólida camada monetária na internet, fazendo a ponte entre as finanças tradicionais e a crescente economia digital. Trata-se de um instrumento para enviar, gastar, poupar, armazenar e liquidar valor, além de gerenciar os riscos nos mercados globais disponíveis 24 horas por dia, 7 dias por semana. Com a entrada em vigor de uma supervisão prudencial rigorosa dos emissores de stablecoins em vários mercados ao redor do mundo — incluindo os EUA —, o crescimento recente das stablecoins regulamentadas é particularmente digno de nota. O crescimento da participação de mercado do USDC acelerou de modo significativo, atingindo 29% das stablecoins em circulação4 e 40% do volume de transações de stablecoins.5 O USDC já viabilizou mais de US$ 50 trilhões acumulados em liquidações on-chain.6

Participação de mercado do USDC

Stablecoins em circulação (US$ bi)

Volume de transações em stablecoins (US$ tri)

Stablecoin transaction volume ($T)

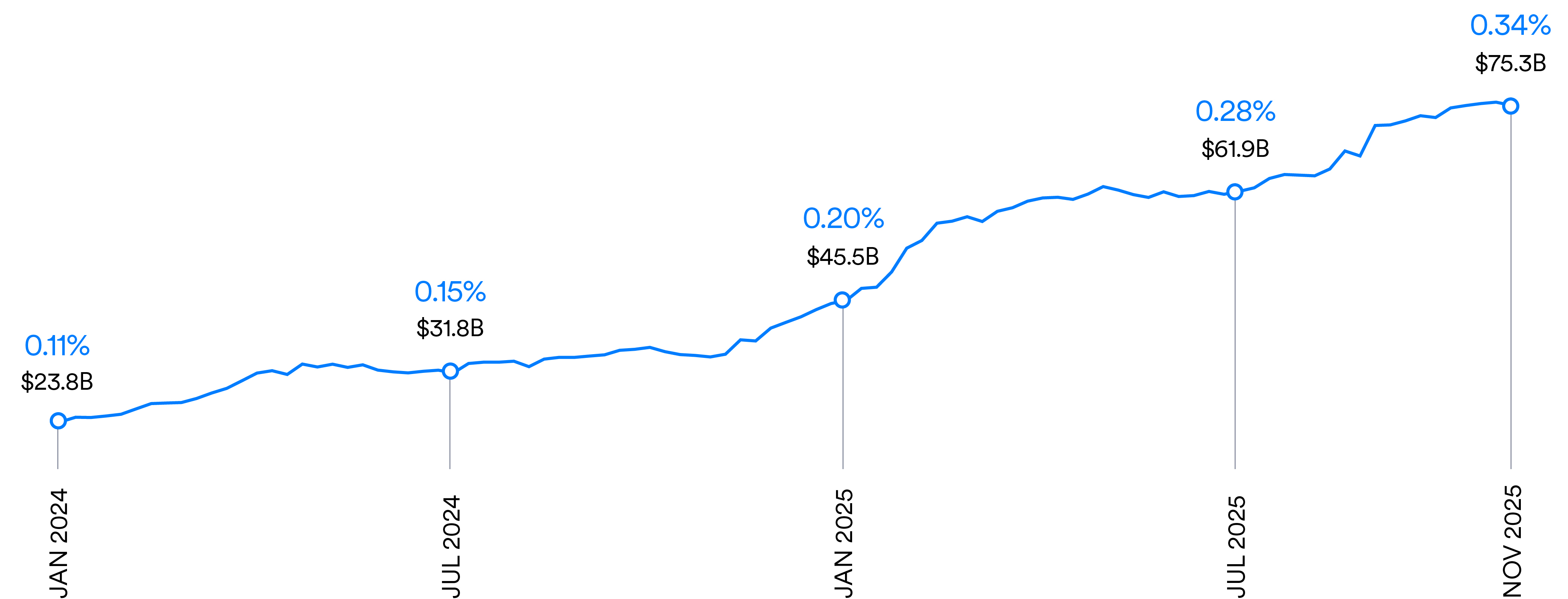

Em uma perspectiva mais ampla, a participação do USDC no agregado monetário M2 também está aumentando cada vez mais rapidamente.7

Stablecoins como uma parcela do M2

Embora mais de 90% das stablecoins sejam denominadas em dólares americanos, o volume das stablecoins não denominadas em dólares também está começando a aumentar. O volume em circulação do EURC, a stablecoin da Circle denominada em euros, aumentou mais de oito vezes8 desde que o abrangente marco regulatório MiCA (Mercados de Criptoativos) da União Europeia começou a ser aplicado no final de junho de 2024. O MiCA define regras claras para os emissores de stablecoins e regula suas ofertas como tokens de dinheiro eletrônico, criando uma infraestrutura quase equivalente às bem-conhecidas estruturas de dinheiro eletrônico e dinheiro móvel. Ao mesmo tempo, preserva os recursos abertos únicos das stablecoins e suas respectivas redes blockchain.

O EURC é uma stablecoin lastreada em euros globalmente acessível, em conformidade com o MiCA e emitida pela Circle sob um modelo de reserva total semelhante ao do USDC. As reservas denominadas em euros são mantidas em instituições financeiras regulamentadas no Espaço Econômico Europeu (EEE), com atestados publicados mensalmente. O EURC é a principal stablecoin de euro em circulação, com uma participação de mercado de mais de 50%,⁹ e costuma ser usado para negociações de câmbio, além da tomada e concessão de empréstimos.

A tokenização de títulos do governo também está começando a se expandir, com mais de US$ 8 bilhões em fundos tokenizados já em circulação, incluindo US$ 1 bilhão em USYC, o fundo de mercado monetário tokenizado (TMMF) emitido pela Circle.10 Esses fundos complementam as stablecoins na qualidade de instrumentos seguros que oferecem rendimentos e também podem ser guardados e movimentados em uma infraestrutura aberta programável, ampliando as possibilidades para tesoureiros, gestores de ativos e instituições financeiras que buscam liquidez, retorno sobre os investimentos e eficiência de capital.

O USYC é um fundo de mercado monetário tokenizado (TMMF) que oferece resgates em USDC quase instantâneos 24 horas por dia, 7 dias por semana. Essa disponibilidade e fungibilidade always-on com dinheiro tokenizado oferecem um utilitário aprimorado se comparado aos fundos tradicionais do mercado monetário, sujeitos às limitações do expediente bancário e das sessões de trading.

Em conjunto, esses fatores demonstram como a clareza regulatória inaugurou uma nova fase para o dinheiro tokenizado: regulamentado, institucional e estrategicamente crucial, com as stablecoins em seu cerne. Quase todos os grandes bancos, empresas de pagamentos, gestores de ativos e corretoras estão avaliando uma estratégia de stablecoins no momento, ponderando se devem comprar infraestrutura, desenvolvê-la por conta própria ou fazer parceria com um emissor estabelecido que já tenha obtido conectividade, liquidez e efeitos de rede profundos, com centenas de milhões de endpoints conectados à internet.

Com o USDC, o USYC, o EURC e a cadeia de valor aberta inerente ao sistema financeiro online, muitas das maiores empresas do mundo estão optando por desenvolver usando nossa infraestrutura como base por meio de parcerias, em vez de criar uma nova stablecoin que enfrentaria problemas de inicialização a frio e altos custos operacionais e de conformidade recorrentes.

As instituições não constroem seus próprios data centers nem desenvolvem seus modelos de linguagem grande para participar da revolução da IA. Ao contrário, desenvolvem em plataformas já estabelecidas, e o mesmo se aplica às stablecoins.

No âmbito do GENIUS Act e das regras promulgadas anteriormente na Europa, no Japão, em Hong Kong e em Abu Dhabi, lançar uma stablecoin de pagamentos em conformidade regulatória não é o mesmo que disponibilizar um novo produto de software. Ao contrário, requer uma infraestrutura consistente de gestão de reservas, relatórios transparentes, operações de tesouraria em tempo real, integrações bancárias e distribuição global em grande escala, para não mencionar uma base sólida de recursos operacionais e de conformidade. O padrão operacional definido pelos reguladores é alto. As stablecoins regulamentadas desfrutam de uma crescente aceitação e efeitos de rede, fornecem elos cruciais entre serviços financeiros nativos da internet e se beneficiam de uma profunda conectividade com o sistema bancário.

Confira como a Circle atua para criar parcerias de stablecoins mutuamente benéficas.

Distribuição e efeitos de rede profundos

Assim como o dólar americano se tornou a moeda de facto para os negócios globais, as stablecoins são, fundamentalmente, um modelo de negócio baseado nos efeitos de rede conforme a Lei de Metcalfe, segundo a qual o valor de uma rede aumenta à medida que mais nós são adicionados. O aumento do número de usuários, a liquidez e a circulação criam uma utilidade, que, por sua vez, atrai mais usuários e aprofunda o valor da rede. Ao mesmo tempo, a natureza de código aberto da cadeia de valor do USDC — juntamente com os serviços de plataforma da Circle, como a Arc, a CPN e a infraestrutura de carteiras digitais — favorece uma onda global de inovação impulsionada por desenvolvedores.

O USDC apresentou um forte crescimento em termos de circulação, liquidez e uso, tanto antes quanto depois do GENIUS Act. A Circle oferece aos parceiros a capacidade de plugar-se diretamente a um ecossistema próspero e em rápido crescimento — composto de usuários corporativos, institucionais e de varejo no mundo inteiro. Nesse diapasão, stablecoins regulamentadas como o USDC e sua cadeia de valor equivalem a um shareware de serviços financeiros: qualquer pessoa pode desenvolver na rede, mas nem todo mundo precisa arcar com o custo de sua manutenção.

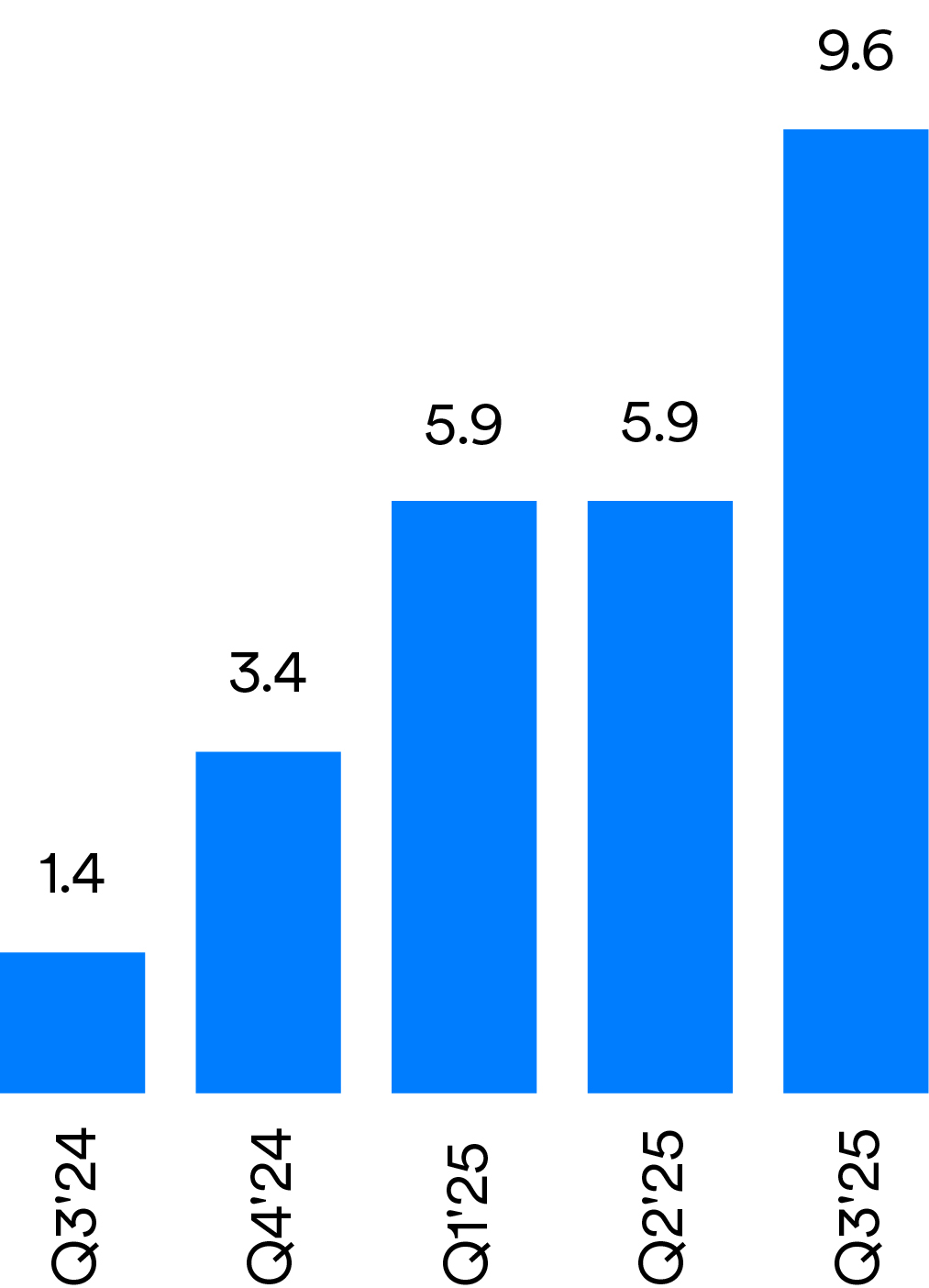

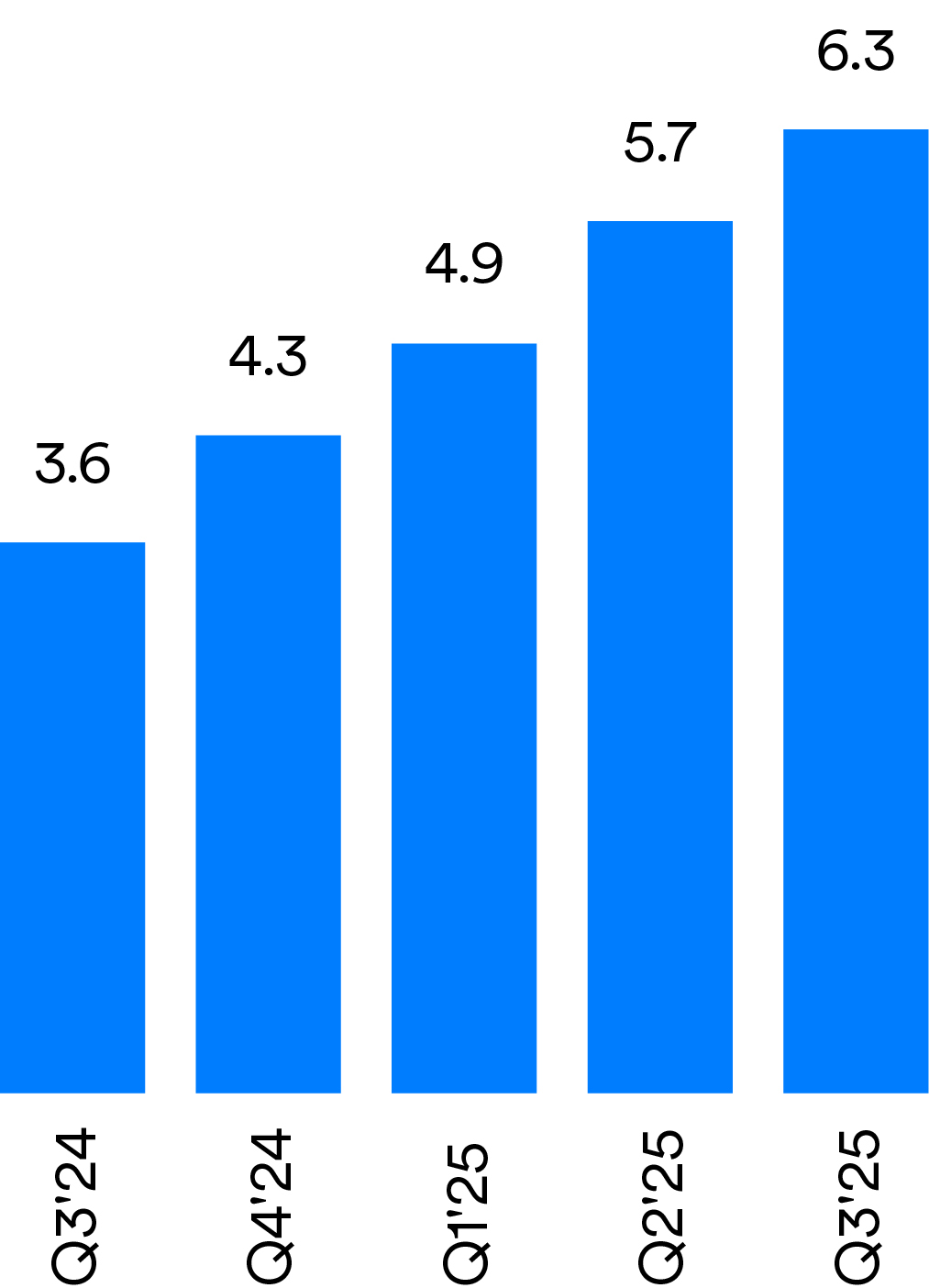

Efeitos de rede do USDC¹²

Volume de transações do USDC on-chain (US$ tri)

Carteiras digitais significativas (M)

Stablecoin transaction volume ($T)

A Circle estabeleceu escala de rede ao trabalhar com seus principais parceiros de distribuição, que disponibilizam USDC para uma ampla gama de usuários. Desde o lançamento do USDC em 2018, a Circle uniu forças com bancos, neobancos, fintechs, empresas de pagamento, corretoras de ativos digitais, gestores de ativos e outros para disponibilizar o USDC diretamente a centenas de milhões de usuários globalmente.

O Standard Chartered é um dos primeiros bancos a adotar stablecoins regulamentadas e ativos digitais estrategicamente para modernizar serviços financeiros. Essa abordagem voltada para o futuro fica evidente em seu próprio ecossistema, que inclui o lançamento de uma empresa de custódia de ativos digitais de nível institucional e a oferta de serviços de spot trading para os principais ativos digitais.

O relacionamento entre o banco e a Circle, que começou em 2023, evoluiu para se tornar um pilar fundamental dessa estratégia. Essa colaboração se expandiu de modo significativo, para além da atuação do Standard Chartered como um parceiro global de gestão de caixa da Circle e, agora, inclui a capacidade do banco de custodiar USDC em blockchains sem permissão e fornecer recursos de cunhagem do USDC, viabilizando um ecossistema de ativos digitais mais coeso tanto para os clientes da Circle quanto do Standard Chartered.

"Nosso trabalho é fornecer acesso ao que nossos clientes consideram importante", afirmou Bill Winters, diretor executivo de grupo do Standard Chartered. "Cada vez mais, nossos clientes querem operar com stablecoins, ativos digitais e blockchain nessa economia incrivelmente eficiente baseada na internet. Juntamente com a Circle e outros parceiros, estamos institucionalizando partes da cadeia de valor da nova economia para podermos proporcionar os benefícios aos nossos clientes e ao mercado mais amplo".

Standard Chartered

Cada vez mais, nossos clientes querem operar com stablecoins, ativos digitais e blockchain nessa economia incrivelmente eficiente baseada na internet.

Integração bancária global

Uma integração profunda com o sistema bancário é essencial, tanto para sustentar as operações com stablecoins nos vários ciclos de mercado quanto para criar escala para um uso global generalizado. A Circle trabalha em estreita colaboração com muitos bancos ao redor do mundo, desde Bancos Globais Sistemicamente Importantes (GSIBs) até bancos regionais, que fornecem uma infraestrutura crucial para garantir que as reservas do USDC sejam gerenciadas adequadamente e a liquidez esteja prontamente disponível no mundo inteiro. Nosso sólido relacionamento com o panorama bancário global é fundamental para a disponibilidade do USDC.

O Deutsche Bank, uma das maiores instituições financeiras do mundo, já é um parceiro bancário da Circle na Europa — uma parceria que é o resultado de uma visão estratégica de longo prazo. O Deutsche Bank reconheceu que fornecer serviços aos emissores de stablecoins regulamentadas poderia agregar um enorme valor e começou a aprimorar sua estrutura de gestão de riscos proativamente para se adaptar a esse novo modelo de negócios.

A aprovação do MiCA, o marco regulatório da Europa, proporcionou um momento crucial de clareza para essa estratégia. A classificação do USDC e EURC pelo MiCA como tokens de dinheiro eletrônico forneceu uma estrutura de supervisão clara no âmbito da Autorité de Contrôle Prudentiel et de Résolution (ACPR), a Autoridade Francesa de Supervisão Prudencial e Resolução. O Regulamento MiCA forneceu ao Deutsche Bank as informações úteis necessárias para construir uma estrutura de risco dedicada para o fornecimento de serviços bancários aos emissores de stablecoins, centrada particularmente na gestão de caixa. Esse impulso inicial na Europa agora está atuando como um modelo para a expansão global, já que o banco está tomando as providências para estender esse acordo a outras jurisdições, incluindo Singapura e os Estados Unidos.

O envolvimento do Deutsche Bank vai além de seus próprios produtos e serviços de gestão de caixa: está contribuindo para dar forma a padrões de conformidade ainda em evolução para o setor de stablecoins. Como participante ativo do Grupo Wolfsberg, uma associação de 12 bancos globais focada na gestão de riscos de crimes financeiros, o Deutsche Bank foi um dos principais colaboradores do "Guidance do Grupo Wolfsberg para a prestação de serviços bancários a emissores de stablecoins lastreadas em moeda fiduciária".13 Trata-se de um trabalho crucial para o desenvolvimento das estruturas harmonizadas necessárias para desbloquear todo o potencial das stablecoins, ao facilitar sua adoção por bancos e outras instituições financeiras tradicionais.

Para o Deutsche Bank, fornecer serviços bancários essenciais dentro de uma estrutura organizada é o primeiro passo para ajudar seus próprios clientes a aproveitar os benefícios das stablecoins, incluindo a programabilidade e uma liquidação global quase instantânea. "As stablecoins representam uma forma completamente nova de pensar sobre valor financeiro", afirmou Ole Matthiessen, codiretor do Banco Corporativo do Deutsche Bank. Pela primeira vez na história, temos à disposição formas reguladas de dinheiro nativo da internet que podem complementar os trilhos de pagamento existentes e criar uma ponte para um futuro em que muitas formas de ativos tokenizados coexistam e gerem sinergias. Estamos ansiosos para promover essa visão em conjunto com a Circle".

O Deutsche Bank já está colocando essa visão em ação. O banco atua como um parceiro de design ativo para as plataformas de última geração da Circle — incluindo a Arc e a CPN —, ajudando a desenvolver a infraestrutura para a era das finanças nativas da internet e permitindo o uso de stablecoins como um mecanismo de compensação alternativo, em particular no caso de pagamentos transfronteiriços. O Deutsche Bank está progredindo em seus planos de lançar uma solução harmonizada de custódia de ativos digitais e stablecoins, que incluirá recursos de custódia e transferência de USDC e EURC. Paralelamente, como parte desses serviços, o Deutsche Bank também está desenvolvendo recursos de suporte à conversão de stablecoins regulamentadas em moeda fiduciária e vice-versa.

Pela primeira vez na história, temos à disposição formas reguladas de dinheiro nativo da internet que podem complementar os trilhos de pagamento existentes e criar uma ponte para um futuro em que muitas formas de ativos tokenizados coexistam e gerem sinergias.

Uma plataforma tecnológica sólida

À medida que a tecnologia subjacente vai sendo cada vez mais relegada ao segundo plano, as stablecoins e o sistema financeiro da internet estão se integrando mais organicamente à infraestrutura financeira tradicional. Tendo isso em mente, a Circle desenvolveu em torno do USDC uma plataforma sólida, que destaca sua neutralidade de rede e facilidade de uso, tornando o USDC particularmente atraente para desenvolvedores e empresas que quiserem criar novos serviços baseados em USDC com a plataforma de produtos da Circle. Esses produtos e a facilidade para desenvolver com USDC o tornam particularmente adequado para atuar como um padrão neutro compartilhado para os dólares na internet.

Parcerias são o caminho mais rápido

Regulamentações rigorosas nos principais mercados deslancharam um "momento stablecoin" para casos de uso convencionais. Instituições financeiras tradicionais e corporações que se mantêm à margem correm o risco de ficar para trás em relação aos concorrentes que estão começando a tirar proveito dessa migração das finanças para as plataformas na internet. A Circle está pronta para ajudar seus parceiros a efetuar essa transição. Saiba mais sobre o que sustenta a rede de stablecoins do USDC, e como se tornar nosso parceiro para aproveitar os profundos efeitos de rede do USDC.

4. Fonte: CoinMarketCap em 30 de setembro de 2025. Stablecoins incluem USDC, USDT, TUSD, PYUSD, RLUSD, USDG, FDUSD e AUSD. Participação é definida como a quantidade de USDC em circulação como um percentual do total de stablecoins de dólar americano lastreadas em moeda fiduciária com circulação acima de US$ 100 milhões, de acordo com o CoinMarketCap.

5. Fonte: Visa Onchain Analytics.

Volume acumulado das transações on-chain do USDC em 18 de dezembro de 2025. Consulte USDC.com.

7. Origens: USDC.com, The Federal Reserve Bank of St. Louis.

8. Em 18 de novembro de 2025; acesse https://www.coingecko.com/en/coins/eurc/eur.

9. Em 18 novembro de 2025; acesse https://defillama.com/stablecoins?pegtype=PEGGEDEUR.

10. Em 18 de novembro de 2025; acesse https://app.rwa.xyz/treasuries.

11. USYC é um token de ativo digital. Cada token de USYC é a representação digital de uma cota do International Short Duration Yield Fund Ltd. da Hashnote (o "Fundo"), um fundo mútuo registrado nas Ilhas Cayman. O Fundo nomeou a Circle International Bermuda Limited ("CIBL"), uma empresa de ativos digitais licenciada pela Autoridade Monetária das Bermudas, como sua administradora de tokens, responsável pela gestão do USYC em nome do Fundo.

12. Fonte: dados da empresa. Observação: "Carteiras Digitais Significativas" são definidas como o número de carteiras digitais on-chain com um saldo de USDC acima de US$ 10.

Valores referentes ao final do período.

13. Confira o documento original "Wolfsberg Group Guidance on the Provision of Banking Services to Fiat-backed Stablecoin issuers".

Esse comunicado de marketing foi emitido pela Circle Internet Financial Europe SAS, uma Instituição de Dinheiro Eletrônico licenciada sob o n° 17788 e uma Provedora de Ativos Digitais registrada na França sob o n° E2024-111.

Os white papers relacionados a tokens de dinheiro eletrônico ("EMT") que emitimos no Espaço Econômico Europeu (EEE) são publicados e disponibilizados no nosso site. Os titulares de EMT têm o direito de resgatá-lo junto ao emissor a qualquer momento na paridade de 1:1.

Contatos: Web: https://www.circle.com | E-mail: [email protected] | Telefone: +33 (1) 59000130